Project Brief

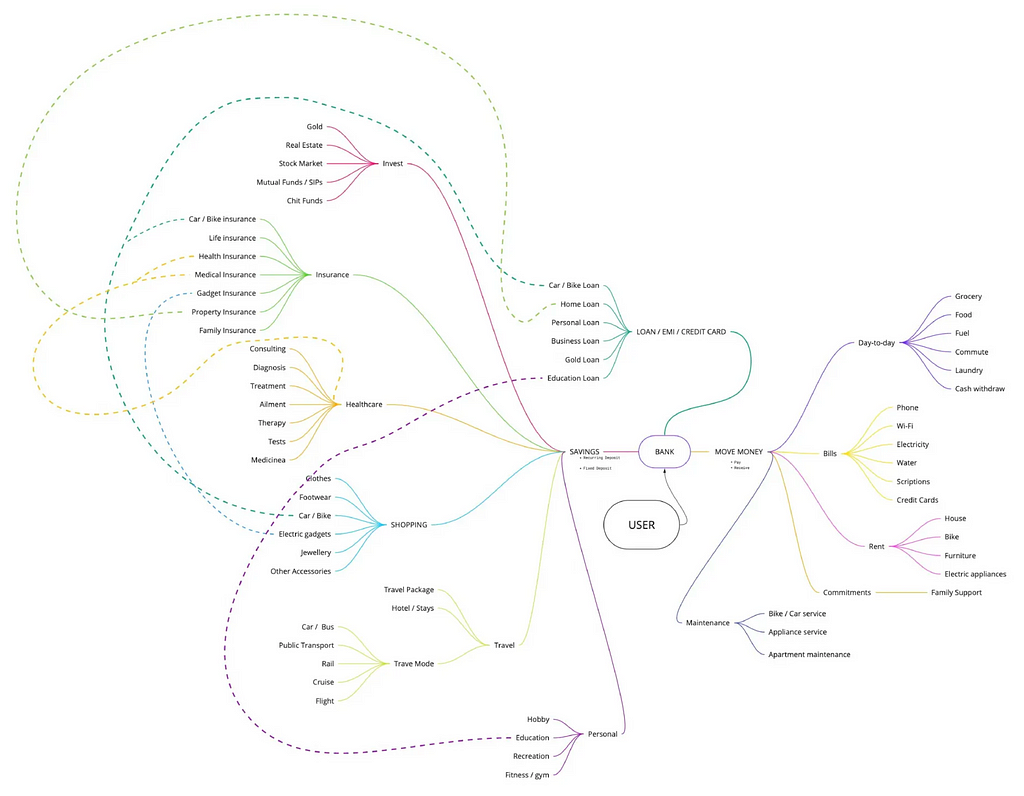

The project involves creating a comprehensive finance management app. It will integrate live shopping updates, investment tracking, credit and debit card transactions from multiple banks, bill management, goals tracking, insurance and loan details, tax calculations, and insights on optimising savings. The app will also provide news and educational content on investments, maturity details for FDs and RDs, and statistical spending insights. Users can perform various financial transactions such as self-transfer, payments to contacts, and UPI-based payments and receive guidance on managing expenses through savings and investments.

Why this Industry

The finance industry presents a compelling opportunity for designing applications due to the significant and widespread challenges outlined in the problem statement. Addressing these issues through innovative and user-friendly applications can transform individuals, businesses, and the overall economic landscape.

Here are some reasons why focusing on the finance industry for designing applications is crucial:

Large Addressable Market

- The problem size indicates that a substantial portion of the Indian population around 70% faces difficulties in managing personal finances. Developing applications that cater to this large market can have a widespread positive impact.

Social Impact

- Improving access to efficient finance management tools can reduce financial stress and improve individuals’ overall well-being. By promoting financial literacy and providing tools for effective budgeting and planning, the application can empower users to make informed financial decisions.

Economic Growth

- The absence of robust finance management tools not only affects individuals but also has broader implications for economic growth. Enabling better financial management can lead to increased savings, investments, and overall economic stability.

Opportunity for Innovation

- The challenges outlined in the additional insights, such as inefficient investment practices, limited financial literacy, and complexities in business financial management, present opportunities for innovative solutions. Designing applications that address these specific pain points can set the stage for groundbreaking solutions.

Technology Adoption

- With the increasing penetration of smartphones and internet connectivity, there is a growing opportunity to leverage technology for financial inclusion. Mobile applications can provide a convenient and accessible platform for users to manage their finances.

Business Growth and Sustainability

- Small businesses face challenges in financial reporting, cash flow management, and accessing funding. Developing applications that cater to the unique needs of small businesses can contribute to their growth and long-term sustainability.

Long-Term Impact

- Inadequate retirement planning is a significant concern. Applications that assist individuals in planning for their retirement can have a lasting impact on their financial security and well-being in later years.

Government Initiatives

- Governments and regulatory bodies often encourage initiatives that promote financial inclusion and literacy. Aligning with such initiatives can support and recognise applications designed to address financial challenges.

Problem Statement

Problem

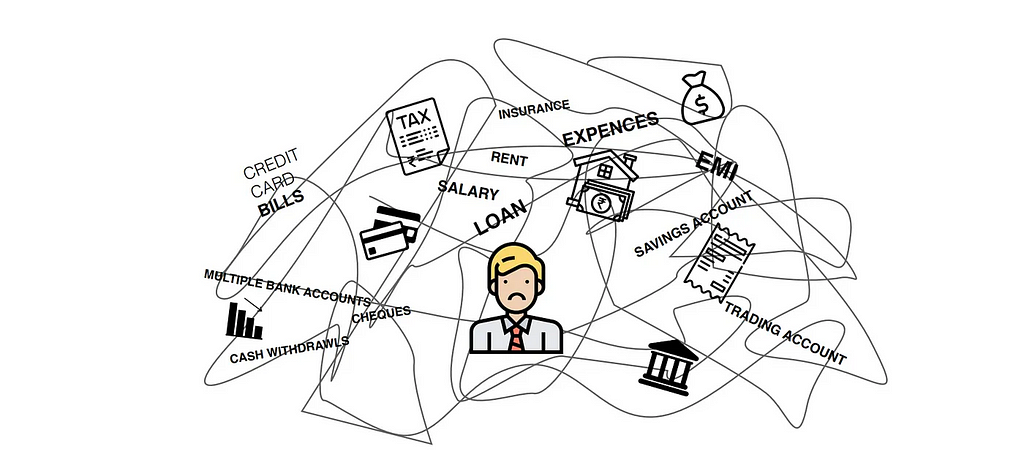

- Traditional banking apps create fragmented financial experiences, forcing users to juggle various tools for banking, loans, expenses, and taxes. This results in inefficiencies, data disarray, and security risks. Many in India lack access to efficient finance tools, hindering budgeting and long-term planning.

Problem Size

- Around 70% of individuals in India struggle with personal finance management. A broad survey of finance app users reveals a 50% dissatisfaction rate with current tools

Problem Impact

- The absence of robust finance tools causes stress, hindering savings and economic growth. The finance management app could increase user satisfaction by 35% through customization.

- Improved financial literacy features may reduce decision-making stress by 25%, while enhanced investment tools could boost financial independence by 20%.

- Small businesses might see a 30% increase in success, user-friendly budgeting tools could reduce stress by 40% for homemakers, and retirement planning enhancements may cut stress by 15% for retirees.

Competitors SWOT Analysis

Mint Intuit

Strengths:

- Established brand with trust.

- Automated, real-time expense tracking.

- Clean and intuitive user interface.

- Bank-level security for user data.

Weaknesses:

- Limited investment tracking features.

- Basic financial reports.

Opportunities:

- Enhance investment tracking.

- Expand financial reporting capabilities.

Threats:

- Intense competition from emerging FinTech apps.

- Rapid technological advancements impacting features.

Money Lover

Strengths:

- Feature-rich budgeting tool with expense tracking, budget planning, and bill reminders.

- Multi-currency support for users with international financial activities.

- In-app financial analytics and reports for better insights.

Weaknesses:

- Some advanced features may require a premium subscription, limiting access for free users.

- The user interface may not be as intuitive as some competitors.

Opportunities:

- Integration with additional financial institutions for automatic transaction syncing.

- Collaborations with other financial apps for a more comprehensive financial management experience.

Threats:

- Stiff competition from established players and emerging FinTech apps.

- Changes in financial regulations affecting data aggregation capabilities.

Niyo Money (formerly ET Money)

Strengths:

- Comprehensive investment tracking with mutual funds, SIPs, and insurance tracking.

- Integration with bank accounts for seamless expense tracking.

- User-friendly interface with goal-based financial planning.

Weaknesses:

- Relatively lower brand recognition compared to traditional financial institutions.

- Limited support for international financial activities.

Opportunities:

- Expansion of services beyond investment tracking to compete with all-in-one financial apps.

- Collaboration with wealth management services to enhance the platform’s capabilities.

Threats:

- Competition from both FinTech startups and traditional financial institutions.

- Technological disruptions impacting the fintech landscape.

QuickBooks

Strengths:

- Established a brand with a user-friendly interface.

- Comprehensive features and integration with Intuit.

Weaknesses:

- Perceived high cost for smaller businesses.

- The learning curve for users with limited accounting experience.

Opportunities:

- Continuous improvement and user feedback.

- Global expansion and AI integration.

Threats:

- Intense competition from FinTech startups.

- Regulatory changes and technological advancements.

Summary

- Mint Intuit: Known for its trust and automation but needs improvement in investment tracking and financial reporting.

- Money Lover: Offers a user-friendly experience with customizable budgets, but reporting features and investment tracking can be enhanced.

- Niyo Money (formerly ET Money): Excels in comprehensive investment tracking and seamless expense management but faces challenges with brand recognition and limited support for international financial activities.

- QuickBooks: Professional and feature-rich with advanced tools, but the subscription cost may be a challenge for some users.

Stakeholder Analysis

Target Audience

- Age Group: Identify the age range of potential users. For a finance management app, it might be adults in the age range of 21 to 60 years

- Occupation: Consider professionals, business owners, or anyone who needs to manage their finances regularly.

- Income Levels: Consider individuals with varying income levels, from middle-income to high-income groups.

- Education Level: Determine the educational background of the target audience, as this can influence their financial management needs and understanding.

- Tech Savviness: Assess the level of technological proficiency of the users. Ensure that the app is user-friendly for both tech-savvy individuals and those who may be less familiar with technology.

- Financial Literacy: Consider the financial literacy levels of the target audience. The app may need to cater to both individuals with a strong understanding of finance and those who are less financially literate.

- Cultural Factors: Understand cultural nuances and preferences related to financial management in the Indian context. Different regions in India may have varying financial habits and practices.

- Language Preferences: Take into account the diverse linguistic landscape in India. Ensure that the app supports multiple languages to cater to a broader audience.

- Mobile Device Usage: Given the widespread use of smartphones, consider individuals who use mobile devices for financial management. Ensure that the app is optimized for mobile platforms.

- Financial Goals: Identify common financial goals among the target audience, such as savings, investments, budgeting, and tax planning.

- Accessibility: Consider accessibility features to ensure that the app can be easily used by individuals with diverse abilities.

User Interview Questions

Persona 1: Tech-Savvy Professional

Q: In what ways do you envision real-time financial insights making a significant impact on your decision-making process regarding investments, wealth management, and tax optimization?

- Real-time financial insights will revolutionize my decision-making. Swift data analysis ensures timely adjustments to my portfolio, adapting wealth strategies dynamically, and optimizing tax planning. It’s the key to staying ahead in the fast-paced financial landscape.

Q: What customization options would you find most valuable in the app to ensure it aligns precisely with your unique financial goals and strategies?

- As a tech-savvy professional, the most valuable customization options for me would include the ability to tailor investment tracking features, set personalized alerts for market changes, and customize reporting dashboards to align precisely with my unique financial goals. Additionally, integration with third-party financial tools and APIs for seamless data flow would enhance the app’s adaptability to my specific strategies.

Persona 2: Small Business Owner

Q: In managing cash flow fluctuations, what specific features or functionalities could simplify the process and ensure better financial stability for your business and what features would be crucial to include in the app to provide the necessary support?

- As a small business owner, key features for managing cash flow fluctuations would include real-time expense tracking, predictive analytics to foresee potential shortfalls, and the ability to set custom budget thresholds. Seamless integration with banking platforms for quick fund transfers and a flexible invoicing system would be crucial. Additionally, the app should offer insights into upcoming expenses and suggest optimized payment schedules. These features would simplify the process, ensuring better financial stability for my business.

Q: When it comes to tax-related processes, what tools or support would you find most helpful in ensuring a more straightforward and efficient experience?

- As a small business owner, having an intuitive tax calculator within the app, automated expense categorization for tax deductions, and real-time updates on tax law changes would be immensely helpful. Seamless integration with accounting software and the ability to generate tax reports easily would ensure a straightforward and efficient tax experience.

Persona 3: Student

Q: Given your goal-oriented financial planning, what features would you like to see in the app to assist you in balancing short-term and long-term financial goals effectively?

- As a college student focused on balancing short-term expenses and long-term goals, I’d appreciate features in the app like a goal tracker with actionable steps, budgeting tools tailored for student life, and personalized savings plans. Additionally, educational content on smart financial habits and investment basics would be beneficial for long-term planning.

Q: What kind of guidance and educational content would be most beneficial to you as a young professional seeking financial independence and future planning?

- As a young college student aspiring for financial independence, I’d find guidance on budgeting for student life, tips for managing student loans, and insights on starting to invest with limited funds highly beneficial. Practical advice on building credit responsibly and navigating entry-level income scenarios would also be valuable for my future planning.

Persona 4: Homemaker

Q: Considering your focus on household budgeting, what features or tools would make the app more user-friendly and supportive in managing family finances efficiently and what frustrations do you commonly encounter with current financial tools?

- As a homemaker, a user-friendly app would ideally offer customizable family budget categories, intuitive expense tracking for various household needs, and automated bill reminders. Tools for setting savings goals and visualizing spending trends would be crucial. Current frustrations include complex interfaces and limited family-centric features in existing financial tools, making efficient household budgeting challenging.

Persona 5: Retired Person

Q: In navigating retirement fund complexities, what specific tools or features would assist you in preserving savings and effectively managing your retirement income?

- As a retired professional, tools that simplify tracking retirement accounts, provide projections on future income, and offer tax-efficient withdrawal strategies would be invaluable. Additionally, features like automated expense categorization and insights into optimizing Social Security benefits would assist in preserving savings and effectively managing my retirement income.

Q: What specific frustrations do you encounter with current retirement-specific tools, and how can the app facilitate communication and collaboration with financial advisors and peers to ensure a stress-free retirement experience?

- Current retirement tools often lack user-friendly interfaces and struggle with comprehensive income projections. The app should streamline communication with financial advisors, allowing easy document sharing and real-time updates. Peer collaboration features could include forums for retirement insights and shared experiences, fostering a supportive community for a stress-free retirement experience.

User Persona

Persona 1: Tech-Savvy Professional

- Age: 25–35 years

- Income: Variable, may have a mix of financial knowledge

- Education: Bachelor’s/Master’s degree

- Problem Statement: Tech-savvy professionals face challenges in managing their investments due to time constraints and a desire for real-time financial insights. The complexity of existing financial tools and the lack of customization options hinder their ability to make informed decisions.

- Problem Size: High-income individuals aged 28–35 show a 70% frustration rate with investment management time, while a data analysis reveals a 50% drop in financial app usage among professionals due to overly complex interfaces.

- Problem Impact: A 60% reduction in investment optimization is observed due to time constraints, impacting financial independence goals for 40% of professionals who face challenges due to a lack of real-time insights.

- Tech Savviness: Comfortable using technology and mobile apps.

- Financial Literacy: Basic financial literacy

- Goals: Investment planning, wealth management, and tax optimization.

- Pain Points: Time constraints managing investments and the desire for real-time financial insights.

- Frustrations: Users struggle with complex financial tools and limited customization, calling for simpler, more personalized solutions.

- Behaviour and Attitude: Proactively seek financial advice and prefer making data-driven decisions.

- Influence: Financial advisors, and industry experts.

- Motivation: Financial independence and growth.

Persona 2: Small Business Owner

- Age: 35–45 years

- Income: Moderate to High

- Education: Varies (typically diploma to degree)

- Problem Statement: Small Business Owners encounter difficulties in managing cash flow fluctuations and simplifying tax-related processes. Existing financial tools often lack support for business-specific finances, leading to frustration and inefficiencies.

- Problem Size: Research suggests that 65% of small business owners face challenges in cash flow management, impacting growth plans, with an additional 40% expressing dissatisfaction with financial software due to a lack of customization for their specific business needs.

- Problem Impact: Improved cash flow management could lead to a potential 30% increase in business success and financial stability, while a 45% reduction in time spent on tax-related tasks could enhance overall productivity.

- Tech Savviness: Comfortable with technology but may not be an expert

- Financial Literacy: Moderate financial literacy

- Goals: Expense tracking, business financial management, and growth planning

- Pain Points: Managing cash flow fluctuations and Simplifying tax-related processes

- Frustrations: Insufficient support for business-specific finances and limited customization for business needs underscore the need for more tailored and comprehensive financial solutions for businesses.

- Behaviour and Attitude: Values practicality and efficiency while preferring straightforward interfaces, emphasizing a preference for streamlined and user-friendly solutions.

- Influence: Accountants, business peers

- Motivation: Business success and financial stability

Persona 3: Student

- Age: 21–25 years

- Income: Pocket money

- Education: Bachelor’s degree

- Problem Statement: Young Professionals with pocket money incomes face challenges in balancing short-term and long-term financial goals. Overly complex financial jargon and a lack of guidance for beginners contribute to frustration and decision-making difficulties.

- Problem Size: Young professionals aged 25–30 express a 50% confusion rate in long-term financial planning, driving a 35% surge in inquiries within online financial communities seeking simplified financial terminology.

- Problem Impact: Improved guidance for goal-oriented financial planning has the potential to bring about a 25% increase in savings, while enhanced financial literacy could contribute to a 40% reduction in decision-making stress among young professionals.

- Tech Savviness: Highly tech-savvy, primarily uses mobile devices

- Financial Literacy: Basic financial literacy

- Goals: Budgeting, savings, and goal-oriented financial planning

- Pain Points: Limited disposable income

- Frustrations: Overly complex financial jargon

- Behaviour and Attitude: Open to learning and experimentation

- Influence: Peers, online financial communities

- Motivation: Financial independence and future planning

Persona 4: Homemaker

- Age: 30–50 years

- Income: Pocket money

- Education: Varies (typically high school to Bachelor’s degree)

- Problem Statement: Homemakers, with variable income and basic financial knowledge, struggle with managing expenses efficiently. Existing financial tools often overwhelm them, and the lack of tailored solutions adds to their frustration.

- Problem Size: Homemakers express a 60% dissatisfaction rate with current budgeting tools, with 45% reporting difficulties in efficiently managing household expenses according to a recent study.

- Problem Impact: Enhanced budgeting tools have the potential to achieve a 50% reduction in financial stress among homemakers, while a 35% increase in overall financial satisfaction is attainable through user-friendly interfaces.

- Tech Savviness: Variable, may be less tech-savvy

- Financial Literacy: Variable, may have basic financial knowledge

- Goals: Household budgeting, savings, and family financial planning

- Pain Points: Limited personal income

- Frustrations: Lack of tailored solutions for homemakers

- Behaviour and Attitude: Values simplicity and practicality

- Influence: Family members, friends

- Motivation: Family financial stability

Persona 5: Retired Person

- Age: 55–70 years

- Income: Pension and savings

- Education: Varies (typically high school to Bachelor’s degree)

- Problem Statement: Retirees, often less comfortable with technology, face challenges in navigating retirement fund complexities. Confusing financial terminology and a lack of retirement-specific tools contribute to their frustrations.

- Problem Size: Retirees face a 40% difficulty rate in understanding retirement fund statements, and dissatisfaction with the lack of retirement-specific features in financial apps is expressed by 55%, highlighting challenges in effective retirement financial management.

- Problem Impact: Enhanced retirement tools may result in a 30% reduction in stress related to financial management for retirees, while a 20% increase in retirement fund comprehension could foster more informed financial decisions in retirement.

- Tech Savviness: Variable, may or may not be comfortable with technology

- Financial Literacy: Variable, may have a mix of financial knowledge

- Goals: Retirement income management, savings preservation, and simplified financial tracking

- Pain Points: Balancing fixed income with expenses

- Frustrations: Lack of retirement-specific tools

- Behaviour and Attitude: Seeks ease of use and reliability

- Influence: Financial advisors, peers

- Motivation: Comfortable and stress-free retirement

User Empathy

Persona 1: Tech-Savvy Professional

Say and Do

- Expresses the need for real-time financial insights and efficient investment tools.

- Actively seeks advice from financial advisors and industry experts.

See

- Views financial management as a strategic and data-driven process.

- Observe trends and market movements through advanced analytics.

Hear

- Engages in discussions with peers and experts about investment strategies.

- Listens to podcasts or attends webinars on financial planning.

Think and Feel

- Thinks about achieving financial independence and growth.

- Feels frustrated with complex financial tools, seeking customization options.

Persona 2: Small Business Owner

Say and Do

- Expresses the need for practical and efficient financial tools for business.

- Actively manages expenses and plans for business growth.

See

- Sees financial management as a crucial aspect of achieving business success.

- Observes how financial decisions impact cash flow and overall stability.

Hear

- Listens to advice from accountants and peers in the business community.

- Engages in discussions on simplifying tax-related processes.

Think and Feel

- Thinks about achieving business success and financial stability.

- Feels frustrated with inadequate support for business-specific finances.

Persona 3: Young Professional

Say and Do

- Expresses the need for user-friendly interfaces for budgeting and savings.

- Actively seeks guidance and information on financial planning.

See

- Sees financial independence as a key goal for the future.

- Observe peers and online communities for financial tips.

Hear

- Listens to advice from peers and participates in online financial discussions.

- Attends financial literacy workshops or webinars.

Think and Feel

- Thinks about balancing short-term and long-term financial goals.

- Feels frustrated with complex financial jargon and seeks simplicity.

Persona 4: Homemaker

Say and Do

- Expresses the need for simplicity and practicality in financial tools.

- Actively manages household budgets and seeks family financial stability.

See

- Sees financial management as a means to ensure family well-being.

- Observe how expenses impact overall family financial health.

Hear

- Listens to advice from family members and friends on efficient budgeting.

- Engages in discussions on managing expenses efficiently.

Think and Feel

- Thinks about the limited personal income and managing expenses.

- Feels overwhelmed by financial tools and seeks user-friendly interfaces.

Persona 5: Retired Person

Say and Do

- Expresses the need for ease of use and reliability in financial tools.

- Actively manages retirement income and savings.

See

- Sees financial management as a way to ensure a stress-free retirement.

- Observe the impact of fixed income on daily expenses.

Hear

- Listens to advice from financial advisors and peers on retirement planning.

- Engages in discussions on simplifying financial terminology.

Think and Feel

- Thinks about navigating retirement fund complexities.

- Feels frustrated with the lack of retirement-specific tools and seeks simplicity.

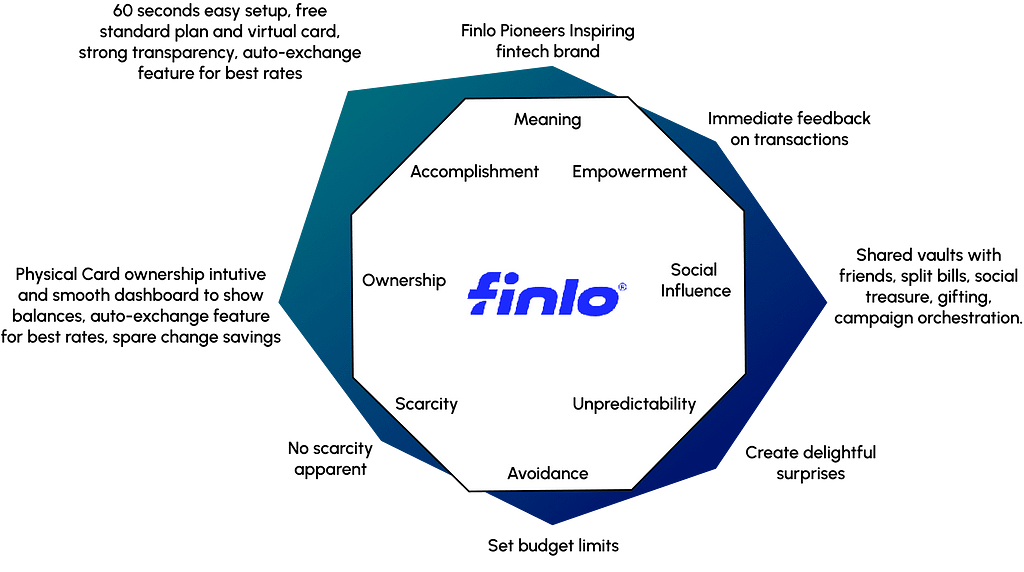

Octalysis Framework

Future enhancements

Big businesses often require more complex and sophisticated financial management applications due to the scale, diversity, and intricacies of their operations. Here are some aspects that contribute to the complexity of financial management for large enterprises:

Multiple Business Units and Entities:

Big businesses may operate across various business units, subsidiaries, or entities. Managing finances at this scale requires the ability to consolidate and analyze financial data from diverse sources.

Global Operations:

Large enterprises often have a global presence, dealing with multiple currencies, tax regulations, and compliance requirements in different countries. The financial management system needs to handle these complexities seamlessly.

Advanced Budgeting and Forecasting:

Big businesses engage in sophisticated budgeting and forecasting processes. The financial application must support advanced modelling, scenario planning, and forecasting to help executives make strategic decisions.

Enterprise Resource Planning (ERP) Integration:

Integration with ERP systems becomes crucial for big businesses. This includes linking financial data with other operational data for a holistic view of the organization’s performance.

Complex Reporting and Analytics:

Large enterprises often require extensive and customizable reporting and analytics capabilities. The financial application must generate detailed financial reports for internal stakeholders, regulatory authorities, and shareholders.

Risk Management:

The complexity of risk management increases with the size of the business. The financial application needs to incorporate robust risk assessment and management features to safeguard the organization’s financial health.

Compliance and Regulatory Requirements:

Big businesses must adhere to a myriad of regulatory requirements and compliance standards. The financial management application must facilitate compliance tracking and reporting to ensure adherence to legal and industry regulations.

Audit Trail and Security:

A comprehensive audit trail and robust security measures are essential for large enterprises. The financial application should provide detailed logs and controls to meet auditing requirements and safeguard sensitive financial data.

Customization and Scalability:

The financial application must be highly customizable to accommodate the unique needs of a large enterprise. Additionally, it should be scalable to handle increased data volumes and user loads as the business grows.

Strategic Financial Planning:

Big businesses engage in strategic financial planning that goes beyond day-to-day operations. The financial management application should support long-term financial strategies and goals.

Articles

Financial Landscape in India:

Understand the current financial landscape in India, including banking systems, regulatory frameworks, and emerging trends.

Challenges in Personal Finance:

Explore articles discussing the common challenges individuals face in managing personal finances in India.

https://www.researchgate.net/publication/269739196_Financial_Literacy_Challenges_for_Indian_Economy

Small Business Financial Challenges:

Investigate the financial challenges small businesses encounter in India, considering aspects like funding, taxation, and cash flow.

Investment Trends and Practices:

Look into articles that highlight investment trends, preferences, and common practices among Indians.

Retirement Planning in India:

Understand the challenges and best practices in retirement planning, considering the demographic shift and increasing life expectancy in India.

https://ijcrt.org/papers/IJCRT2103243.pdf

Case Studies on Successful Financial Apps:

Analyze case studies of successful finance management applications or platforms that have gained traction in the Indian market.

https://www.mdpi.com/2071-1050/14/21/14506

Government Initiatives in Finance:

Learn about government initiatives aimed at promoting financial inclusion and literacy in India.

Digital Payment Trends:

Investigate the latest trends and developments in digital payments, considering the government’s push towards a cashless economy.

Thank you for reading till the end! Did you know? You can hold the clap button for a few seconds to give a maximum of 50 claps. I would appreciate it

I love talking about UI/UX. If you have any feedback or just want to have a casual conversation, reach out to me on LinkedIn.

Here is a link to my Portfolio.

Please take a look at my other articles

Colour psychology to empower and inspire you

![]()

Navigating the future financial landscape was originally published in UX Planet on Medium, where people are continuing the conversation by highlighting and responding to this story.